- Divide your interest rate by the number of payments you’ll make that year. ...

- Multiply that number by your remaining loan balance to find out how much you’ll pay in interest that month. ...

- Subtract that interest from your fixed monthly payment to see how much in principal you will pay in the first month. ...

- For the following month, repeat the process with your new remaining loan balance, and continue repeating for each subsequent month.

How to Calculate Auto Loan Interest for First Payment

- Divide your interest rate by the number of monthly payments you will be making over the course of the year.

- Multiply it by the balance of your loan, which for the first payment, will be your whole principal amount.

Should I finance or pay cash for a car?

This calculator helps you to determine which is best for you—financing or paying cash for a car. Paying cash for your car may be your best option if the interest rate you earn on your savings is lower than the after-tax cost of borrowing. However, keep in mind that while you do free up your monthly budget by eliminating a car payment, you may also have depleted your emergency savings to do so.

How is the interest rate for a car loan calculated?

There are a couple of factors that go into determining this amount:

- Principal Amount: The principal amount is the cost you want to borrow.

- Loan Term: How long you plan on taking to pay off the loan also plays a role. ...

- Repayment Schedule: Usually, you will make a payment on your vehicle every month, but you are able to make payments more often if you prefer. ...

How to calculate a monthly payment on a car loan?

Using the previous loan example of $100,000 at 6%, your calculation would look like this:

- a: $100,000, the amount of the loan

- r: 0.06 (6% expressed as 0.06)

- n: 12 (based on monthly payments)

How do they calculate APR on a car loan?

How Do They Calculate Your Car Loan APR. The annual percentage rate calculated on your car loan is found by taking the rate per period multiplied by the number of payments you will make in a given year. Annual percentage rate is one way to determine the actual expense of financing in a given year, but it is not always the most accurate.

How do I figure out how much interest I will pay on my car loan?

This is done by subtracting your principal from the total value of your payments. To get your total value of payments, multiply your number of payments, "n," by the value of your monthly payment, "m." Then, subtract your principal, "P," from this number. The result is your total interest paid on your car loan.

How do you find the total amount of interest paid over the course of the loan?

Divide the first sum by the second sum. Multiply the amount gained by the total amount of the principal, giving you the payment per month. Multiply the monthly payment amount by the number of months of the loan to get the total amount you have to pay back over the loan term, including interest.

What is the total interest paid over the life of the loan?

Total interest is the sum of all interest paid over the life of a loan or interest-bearing account, including compounded amounts on unpaid accumulated interest. It can be derived using the formula [Total Loan Amount] = [Principle] + [Interest Paid] + [Interest on Unpaid Interest].

How do you enter a formula to calculate the total paid over the life of the loan in Excel?

Select the cell you will place the calculated result in, type the formula =CUMIPMT(B2/12,B3*12,B1,B4,B5,1), and press the Enter key.

How to find the APR of a loan?

Step 1: Find the APR section. Read your loan agreement where it will state the exact interest rate for your loan. It is listed as the APR or Annual Percentage Rate. Tip: Seek loans with a low APR. The lower the APR, the less you pay in interest over the lifetime of the loan.

How long does a car loan last?

Step 2: Find out the length of the loan term. Many car loans for new or slightly used vehicles carry a term up to five or even six years. Some may go as long as seven years, but keep in mind that you pay more interest for longer-term loans.

What is the first step in the loan process?

The first step of the loan process is determining which loan you want to pursue. This requires you to figure out how much you can expect to pay in principal, annual percentage rate (APR), and other fees.

Where to find APR on car loan?

You can find the Annual Percentage Rate (APR) on the disclosure form section of the loan agreement you have to sign when applying for a car loan.

How long does a car loan last?

The term of the loan can range from 24 months to 84 months. The longer the loan term, the more interest you pay. Also, paying off a car loan early usually results in penalties from the lender, so check before doing so. Step 3: Determine the interest rate.

How to calculate monthly payment on a mortgage?

Divide the first sum by the second sum. Multiply the amount gained by the total amount of the principal, giving you the payment per month. Multiply the monthly payment amount by the number of months of the loan to get the total amount you have to pay back over the loan term, including interest.

What is principal owed?

The principal owed represents the amount of money you want to finance. The principal includes the total amount you have to pay for the car minus any rebates, the value of any vehicles you trade in, and the amount of the down payment.

How is car interest calculated?

With a simple interest loan, your interest is calculated based on your loan balance on the day your car payment is due. The amount of interest you pay each month changes. On a car loan with precomputed interest, the interest is calculated at the start of your loan and based on your total loan amount. The amount of interest you pay each month ...

What is interest on a car loan?

When you get a car loan, interest is the price you pay to borrow money from the lender. You must repay the amount you borrow plus interest in monthly payments over the life of the loan. A variety of factors, including how the interest is calculated, your credit scores, the loan term and the size of your down payment influence your rate.

How to pay less interest on a car loan?

How can I pay less interest on my car loan? 1 0% APR financing — If you have excellent credit and the auto manufacturer’s finance division offers special financing, you may be able to take advantage of 0% APR financing for a certain amount of time. 2 Early repayment — If you have a simple interest loan, you can reduce your interest charges by paying more than the minimum due each month or paying off the balance early. 3 Shorter loan term — Choosing a shorter repayment term will lower the total amount of interest you pay in the long run. But it’ll increase your monthly payments, so be sure you can afford it. 4 Refinance down the road — If interest rates drop or your credit improves after you get your car loan, you may be able to get a lower rate by refinancing.

What is the difference between a simple interest loan and an auto loan?

Most auto loans are simple interest loans, which means that the amount of interest you pay each month is based on your loan balance on the day your payment is due. If you pay more than the minimum due, the interest you owe and your loan balance can decrease. On a simple interest loan, interest is front-loaded and amortized.

Why do lenders charge higher rates?

Lenders may charge higher rates when you put little or no money down. This higher rate is in exchange for the risk that you’ll default on the loan and the lender will be left with a vehicle that’s worth less than you owe.

What is precomputed interest?

Precomputed interest. Some auto loans have precomputed interest, which means the interest is calculated upfront based on how much you’re borrowing. That amount is added to the principal and divided by the number of months in the loan term to determine your monthly payment.

What is the cost of borrowing money?

An interest rate is how much you pay each year to borrow money, expressed as a percentage . APR reflects the interest rate plus any additional loan fees. It’s also expressed as a percentage. A higher APR or interest rate means that more money will come out of your pocket until you pay off the loan in full.

1. The Lender Buys

If you need a loan to purchase a new car, your lender actually purchases the car for you and allows you to pay it back over a period of time. This is not dissimilar to how loans work with homes or even college tuition. Basically, your lender gives you its money, and, in exchange, you compensate the lender for its services by paying interest.

2. Interest is Simple (Usually)

Most car loan lenders (Sioux Falls Federal Credit Union, included) use a simple daily interest to calculate your accruing debt over time. With this type of interest, charges are calculated only on the principal (the original amount owed on a loan). Simple daily interest does not compound on interest, which generally saves you money.

Ready to calculate your own payment amount?

To figure out a new monthly payment, you can utilize our auto loan calculator here.

What does interest rate mean on a car loan?

Interest rate: The cost to borrow the money, expressed as a percentage of the loan.

How to calculate car payment with low credit score?

To calculate your monthly car loan payment by hand, divide the total loan and interest amount by the loan term ( the number of months you have to repay the loan).

How to find the best interest rate?

So, it pays to shop around to find the best rate possible. While interest rates vary by lender, your rate depends on other factors, too, including: 1 Federal Reserve interest rates: When the Fed keeps interest rates low, you pay less to borrow money. 2 Your credit score: In general, the better your credit, the lower your interest rate will be. 3 Your debt-to-income ratio (DTI): Your DTI shows how much of your gross monthly income goes toward paying your monthly debts. The lower your DTI, the lower your interest rate will be. 4 Loan type: Loans for used cars have higher rates than those for new cars (because used cars have a lower resale value). 5 The loan term: Longer loan terms usually have higher interest rates.

What is vehicle cost?

Vehicle cost: The amount you want to borrow to buy the car. If you plan to make a down payment or trade-in, subtract that amount from the car's price to determine the loan amount. Term: The amount of time you have to repay the loan. In general, the longer the term, the lower your monthly payment, but the more interest you will pay overall.

What is total interest paid?

Total interest paid: The total amount of interest you'll have paid over the life of the loan. In general, the longer you take to repay the loan, the more interest you pay overall. Add together the total principal paid and total interest paid to see the total overall cost of the car. Use the auto loan calculator before you head to ...

What happens when the Fed keeps interest rates low?

Federal Reserve interest rates: When the Fed keeps interest rates low, you pay less to borrow money. Your credit score: In general, the better your credit, the lower your interest rate will be. Your debt-to-income ratio (DTI): Your DTI shows how much of your gross monthly income goes toward paying your monthly debts.

Do you pay more interest on a loan when the balance is higher?

The interest you pay each month is based on the loan's then-current balance. So, in the early days of the loan, when the balance is higher, you pay more interest. As you pay down the balance over time, the interest portion of the monthly payments gets smaller.

Interest Rate Factors

Before we learn how to figure interest on a car loan, it’s important to understand the basics of what an interest rate is and the factors that affect it. When you take out a loan, you use credit to purchase a vehicle. The lender then technically owns the vehicle until you pay it off.

How to Figure Interest On a Car Loan for the First Payment

Your first payment will be slightly different from all of the rest of your payments on your auto loan. Here’s how you figure out how much your first payment will cost:

How to Calculate Auto Loan Interest Going Forward

After you make your first payment, you’ll then need to determine how much you’ll pay going forward. If you’re like many Sevierville drivers who are new to taking out a loan, here’s how to do it:

Get Your Finance Questions Answered at Ole Ben Franklin Motors

For more car-buying questions and concerns, reach out to the finance center at Ole Ben Franklin Motors. Contact us online or visit us in Knoxville for a consultation.

How long is a 5 year auto loan?

A loan term is the amount of time a lender agrees to stretch out your payments. So if you qualify for a five-year auto loan, your loan term is 60 months. Mortgages, on the other hand, commonly have 15-year or 30-year loan terms.

How does the amount of money you borrow affect interest?

The more money you borrow, the more interest you’ll pay . “For larger loans, the lender is assuming greater risk.

Why do you have to make more than one payment a month?

If you opt to make payments more frequently than once a month, there’s a chance you could save money . When you make payments more often, it can reduce the principal owed on your loan amount faster . In many cases, such as when a lender charges compounding interest, making extra payments could save you a lot.

What is the repayment amount?

Repayment amount. The repayment amount is the dollar amount you’re required to pay on your loan each month. In the same way that making loan payments more frequently has the potential to save you money on interest, paying more than the monthly minimum can also result in savings.

Why are short term loans less expensive?

Shorter loan terms generally require higher monthly payments, but you’ll also incur less interest because you’re minimizing the repayment timeline. Longer loan terms may reduce the amount you need to pay each month, but because you’re stretching repayment out, the interest paid will be greater over time.

Why is interest rate important?

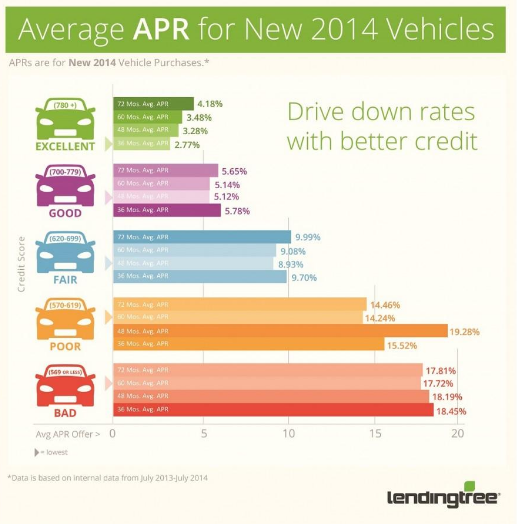

Along with the amount of your loan, your interest rate is extremely important when it comes to figuring out the cost of borrowing. Poorer credit scores typically equal higher interest rates.

Does variable interest rate affect loan?

If it’s variable, your interest costs could rise over the course of your loan and affect your cost of financing. Takeaway: It may make sense to work on improving your credit score before borrowing money, which could increase your odds of securing a better interest rate and paying less for the loan.

Popular Posts:

- 1. which institute is best for medical transcription course in bangalore

- 2. what is financial management course

- 3. what is the best lsat prep course to take

- 4. how to write a college course curriculum

- 5. how long is billing and coding course

- 6. how long is medical assistant course

- 7. what is pmp training course

- 8. what is a course management system

- 9. what is business management course

- 10. how long is hvac course