- School certification Your school must certify your enrollment status with a lender before you can receive a loan. ...

- Minimum borrowing amount As a less-than-half-time student, you probably don’t need to borrow as much money for school as your full-time peers. ...

- Triggering repayment

You can use an Advantage Education Loan if you're enrolled less than half-time, provided you immediately enter repayment, and for non-degree programs like certification courses. Forbearance of 24 months is twice as long as most lenders. Loans are available if you're enrolled less than half time.Apr 4, 2022

Full

AnswerDoes attending college less than half time limit your private student loan options?

Nov 10, 2021 · A few student loan lenders that offer loans to part-time students include: Ascent. College Ave. CommonBond. Sallie Mae. SoFi. Some, like Sallie Mae, even offer loans to students attending less than...

What is considered half time in college?

Apr 18, 2019 · Most private lenders require that borrowers attend at least half time or full time to qualify. Federal direct loan borrowers must be enrolled at …

Do you have to be part time to get a loan?

Apr 23, 2021 · Contact your school’s financial aid office to ask if you have money left over. If so, you may be able to use the remaining funds to cover summer classes. However, you can only use federal student loans if you’ll have at least half-time status, which usually equals three to …

How much can I Borrow for a full time student loan?

Feb 28, 2022 · 1) Talk to Your Financial Aid Office About Summer Financial Aid 2) Look for Grants & Scholarships 3) Apply for a Summer Job or Internship 4) Consider a Private Student Loan Does Federal Financial Aid Cover Summer Classes?

Can I get a student loan for one semester?

Fortunately, you can generally take out private student loans at any point in time. Private lenders are not restricted by the FASFA deadline or semester dates, so you can apply as you need.Dec 21, 2021

What is half time student loan?

6-8 credit hours

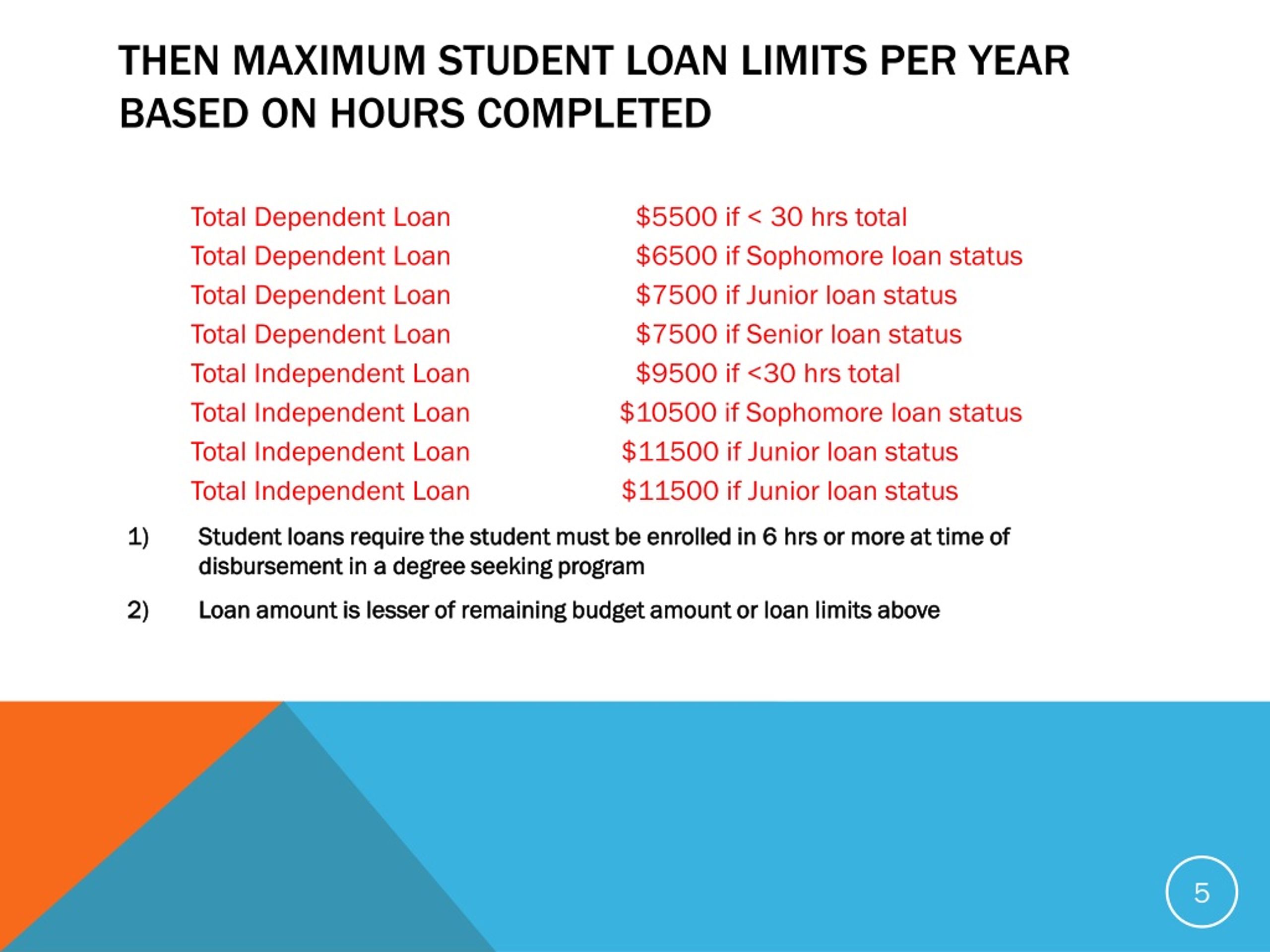

For financial aid purposes, enrollment status for all terms is as follows: full-time is 12 or more credit hours, three-quarter time is 9-11 credit hours, half-time is 6-8 credit hours and less than half-time is 1-5 credit hours.Feb 9, 2016

How many hours do you need to qualify for a student loan?

Generally, students need to be enrolled in a minimum of 6-credit hours to be eligible for financial aid. But, to be eligible for the full financial aid amount, students usually need to be enrolled in 12-credit hours, or be considered full-time students.Mar 30, 2022

How can I get a student loan immediately?

If you need a student loan quickly, you have three main options:

- Borrow up to the federal direct loan limit. Before you consider other loan sources, make sure you're borrowing as much as you can in federal direct student loans. ...

- Explore emergency aid. ...

- Compare private student loan options.

Does financial aid pay for halftime?

You must be enrolled in a degree program and be attending classes full time, half-time, or less than half-time at an eligible school.Feb 28, 2022

Can I get student loans if Im not full-time?

If you would like to borrow Federal Student Loans, you will need to be enrolled at least half-time. If you are awarded a Federal Pell Grant, your school based your award on your financial need, your cost of attendance, your status as a full-time or part-time student, and the length of your program.Apr 10, 2018

Can students take out loans for college?

To apply for a federal student loan, you must first complete and submit a Free Application for Federal Student Aid (FAFSA®) form. Based on the results of your FAFSA form, your college or career school will send you a financial aid offer, which may include federal student loans.

Can I get financial aid if I make over 100k?

4 answers. None of the above for qualifying for Federal Aid. It's 60,000 tops in most cases. It's very rare anyone's family making over $60,000 would qualify for a Pell Grant.

Does fafsa cover part time students?

Part-time students are eligible for federal student loans and grants, as long as they fill out the Free Application for Federal Student Aid (FAFSA). The FAFSA requires that you submit financial information like your income, savings and checking account balances and non-retirement investments.Dec 21, 2020

What are the 4 types of student loans?

There are four types of federal student loans available:

- Direct subsidized loans.

- Direct unsubsidized loans.

- Direct PLUS loans.

- Direct consolidation loans.

Sep 16, 2020

How much can college students borrow?

Undergraduates can borrow up to $12,500 annually and $57,500 total in federal student loans. Graduate students can borrow up to $20,500 annually and $138,500 total. But just because you can borrow that much doesn't mean you should.

Which bank provide education loan easily?

Compare Top Education Loan Offers 2022

| Name of Bank | Interest Rate (p.a.) | Processing Fees |

|---|---|---|

| SBI | 6.70% to 8.65% | Up to Rs.10,000 |

| Axis | 13.70% to 15.20% | Nil to Rs.15,000 + GST |

| Bank of Baroda | 8.85% to 10.85% | 1% of loan amount up to Rs.10,000 |

| HDFC | 9.55% to 13.25% | Up to 1% of loan amount + tax |

How to shop for part time student loans?

How to shop for part-time student loans. Build credit or find a co-signer before you apply for a private student loan. While undergrads generally don’t have the credit history required to get a loan without a co-signer, students over the age of 21 might.

How long do you have to be enrolled in a private school to qualify for a federal loan?

Most private lenders require that borrowers attend at least half time or full time to qualify. Federal direct loan borrowers must be enrolled at least half time. Part-time students enrolled at least half time should start by taking out federal student loans before considering a loan from private lenders.

What banks offer college ad loans?

College Ave Student Loans products are made available through either Firstrust Bank, member FDIC or M.Y. Safra Bank, FSB, member FDIC. All loans are subject to individual approval and adherence to underwriting guidelines. Program restrictions, other terms, and conditions apply. As certified by your school and less any other financial aid you might receive. Minimum $1,000. Rates shown are for the College Ave Undergraduate Loan product and include autopay discount. The 0.25% auto-pay interest rate reduction applies as long as a valid bank account is designated for required monthly payments. Variable rates may increase after consummation. This informational repayment example uses typical loan terms for a freshman borrower who selects the Flat Repayment Option with an 8-year repayment term, has a $10,000 loan that is disbursed in one disbursement and a 7.78% fixed Annual Percentage Rate (“APR”): 54 monthly payments of $25 while in school, followed by 96 monthly payments of $176.21 while in the repayment period, for a total amount of payments of $18,266.38. Loans will never have a full principal and interest monthly payment of less than $50. Your actual rates and repayment terms may vary. This informational repayment example uses typical loan terms for a freshman borrower who selects the Deferred Repayment Option with a 10-year repayment term, has a $10,000 loan that is disbursed in one disbursement and a 8.35% fixed Annual Percentage Rate (“APR”): 120 monthly payments of $179.18 while in the repayment period, for a total amount of payments of $21,501.54. Loans will never have a full principal and interest monthly payment of less than $50. Your actual rates and repayment terms may vary. Information advertised valid as of 10/21/2021. Variable interest rates may increase after consummation. Approved interest rate will depend on the creditworthiness of the applicant (s), lowest advertised rates only available to the most creditworthy applicants and require selection of full principal and interest payments with the shortest available loan term.

How far through your repayment term do you have to be to get a cosigner release?

You must be at least halfway through your repayment term before you can request a co-signer release.

What is Advantage Education Loan?

Advantage Education Loans are fixed-rate loans from the nonprofit Kentucky Higher Education Student Loan Corp. They're available outside Kentucky, but not in every state. You can use an Advantage Education Loan if you’re enrolled less than half-time, provided you immediately enter repayment, and for non-degree programs like certification courses.

When is interest charged on a school loan?

Interest is charged starting when funds are sent to the school. With the Fixed and Deferred Repayment Options, the interest rate is higher than with the Interest Repayment Option and Unpaid Interest is added to the loan’s Current Principal at the end of the grace/separation period.

Do you have to pay interest during grace period?

Payments may be required during the grace/separation period depending on the repayment option selected. Variable rates may increase over the life of the loan. Advertised variable rates reflect the starting range of rates and may vary outside of that range over the life of the loan.

How much does a student loan cost after graduating?

The minimum amount for a private student loan is usually $1,000, and terms range between five and 20 years, depending on the provider.

How much does it cost to take credit hours in college?

The average cost of a credit hour at an in-state college is $396, compared to $1,101 for an out-of-state public school and $1,353 for a private university. If you’re taking two three-credit classes, that’s a difference of between $4,230 and $5,742.

How long does it take to get a private loan?

Private loans are usually faster to obtain than federal loans, and you may be able to receive funding just a few days after being approved. You can also use private loans to cover living expenses, like paying for an apartment, groceries and transportation while you’re taking summer classes.

How to get money for summer classes?

If you know you’ll need money for summer classes, consider applying for scholarships to cover the costs. Start by applying with your university and ask your advisor if there are any special grants or awards available to cover summer classes.

When will student loans be available for summer 2021?

Student Loans for Summer Classes. April 23, 2021. While many college students are gearing up for a summer full of road trips and pool parties, others are stuck preparing for another semester on campus. Whether you’re trying to graduate early or just earning some extra credits to catch up, there’s a good chance you’ll have to take ...

Do parent plus loans stay on credit report?

Unlike other federal student loans, Parent PLUS loans are solely in the parent’s name. They’ll stay on your parent’s credit report until the loan is paid off. Parents who are trying to refinance a house or pay for another child’s college education may be hesitant to take out a Parent PLUS loan for this reason.

Can parents take out parent plus loans?

If you’ve maxed out your student loans, your parents can take out Parent PLUS loans to pay for summer classes. This is your only other federal loan option. Parents can borrow up to the cost of attendance, minus additional aid like scholarships, grants and other loans. As of 2021, the interest rate on Parent PLUS loans is 5.30%.

How long do you have to be enrolled to get financial aid?

Of course, the regular financial aid eligibility requirements apply: You must be enrolled at least half-time and making satisfactory academic progress to qualify.

How to pay for summer classes?

Here are five ways to pay for summer classes. 1. Ask Your Financial Aid Office About Summer Financial Aid. If you’re thinking of taking summer classes, set up an appointment with your school’s financial aid office to see what options you have. They’ll let you know whether the classes you’re interested in are eligible for financial aid.

What is Jamie Johnson's personal finance?

Jamie Johnson writes about a variety of personal finance topics including student loans, credit scores, banking, investing, and personal loans. Her work has been featured on GOBankingRates, Yahoo Finance, and more.

Is there financial aid for summer classes?

Luckily, there are student loans and other types of financial aid available for summer classes. Read on to learn more about your options.

Can you calculate how much FAFSA money you have left over for summer classes?

They’ll let you know whether the classes you’re interested in are eligible for financial aid. They can also help you calculate how much FAFSA money you have leftover for summer classes.

Which type of loan has more benefits?

Loans made by the federal government, called federal student loans, usually have more benefits than loans from banks or other private sources. Learn more about the differences between federal and private student loans.

When do you have to repay federal student loans?

You don’t have to begin repaying your federal student loans until after you leave college or drop below half-time.

How to notify your loan servicer when you graduate?

Notify your loan servicer when you graduate; withdraw from school; drop below half-time status; transfer to another school; or change your name, address, or Social Security number. You also should contact your servicer if you’re having trouble making your scheduled loan payments.

What is the Perkins loan?

A loan is money you borrow and must pay back with interest.

What is a direct subsidized loan?

Direct Subsidized Loans are loans made to eligible undergraduate students who demonstrate financial need to help cover the costs of higher education at a college or career school.

What is complete entrance counseling?

complete entrance counseling, a tool to ensure you understand your obligation to repay the loan; and

How to find out what you are getting paid after graduation?

You can also use the U.S. Department of Labor's Occupational Outlook Handbook or career search tool to research careers and salaries.

How much time does a certificate program take?

Smaller time commitment. Like costs, a certificate program takes much less time than pursuing a graduate degree — usually less than a year. If your schedule has less wiggle room, a certificate program may be much more accessible.

What to look for after filling out FAFSA?

After filling out the FAFSA, you should look for scholarships and grants you might qualify for. Talk to your school’s financial aid office to see if there are any institutional options you might be eligible for. You can also look for scholarships and grants from private organizations, as well as those available through your state.

What happens if you don't go to accredited school?

Lack of accreditation. If you don’t go through an accredited school, your certificate may not be worth what you paid. Check that your program is legit and well respected — and preferably, offered through an accredited institution. May be limiting.

Do you have to have credit to get a federal loan?

It depends. Federal Direct Unsubsidized Loans don’t have credit requirements, but most private lenders do. If you fail to meet your lender’s requirements, see if you can apply with a cosigner to increase your chances of approval.

Is a certificate program worth it?

Poor return on investment. Although a certificate program can be helpful, it may not be worth the cost if you don’t land a high-paying job or have to pay back loans at a high rate. Ensure your program has a good placement rate and is in an industry you love before enrolling.

What does "enrolled" mean in college?

be enrolled or accepted for enrollment as a regular student in an eligible degree or certificate program;

Do you owe money on a federal student loan?

you are not in default on a federal student loan, you do not owe money on a federal student grant, and. you will use federal student aid only for educational purposes; and. show you’re qualified to obtain a college or career school education by.

Do federal student aid programs have their own eligibility criteria?

Some federal student aid programs have their own eligibility criteria in addition to the general requirements listed above. Check with your college’s financial aid office if you have questions about a particular program.

What are the two forms of personal loans?

Personal loans come in two forms: secured and unsecured.

What happens if you don't pay interest on a Perkins loan?

If you choose not to pay the interest while you’re in school, the interest is added to your loan principal, or the total amount you originally borrowed. Perkins loan: The Perkins loan is available for undergraduate, graduate and professional students who have exceptional financial need. Unlike direct loans, with a Perkins loan your school is ...

What is a direct subsidized loan?

Direct subsidized loans: Direct subsidized loans are based on an undergraduate student’s financial need. The federal government pays the interest while you’re in school, so you don’t begin to pay it until you leave school and your grace period ends or are enrolled less than half the time. Direct unsubsidized loans: Undergraduate ...

What is the last resort to pay for school?

Like books and other materials,” he says. “A personal loan should be the last resort to pay for school, as the amount needed to cover tuition is typically much higher than a bank would be willing to lend.”. Personal loans come in two forms: secured and unsecured.

What is a personal loan?

Personal loans are installment loans that can be used to pay for various consumer expenses, like debt consolidation or emergency costs. Some personal loans for students can be put toward education expenses.

What is Direct PLUS loan?

The federal government also offers Direct PLUS loans for graduate or professional students or eligible parents of dependent undergraduates. You can use these loans to pay for the cost of attendance that other financial aid didn’t cover.

How much does higher education cost?

According to the National Center for Education Statistics, the average annual cost (tuition, fees, room and board) for an undergraduate at a public university was $16,757 for the 2015–16 academic year, while at private nonprofit institutions this figure was just over $43,000.

Popular Posts:

- 1. which institute is best for medical transcription course in bangalore

- 2. what is financial management course

- 3. what is the best lsat prep course to take

- 4. how to write a college course curriculum

- 5. how long is billing and coding course

- 6. how long is medical assistant course

- 7. what is pmp training course

- 8. what is a course management system

- 9. what is business management course

- 10. how long is hvac course