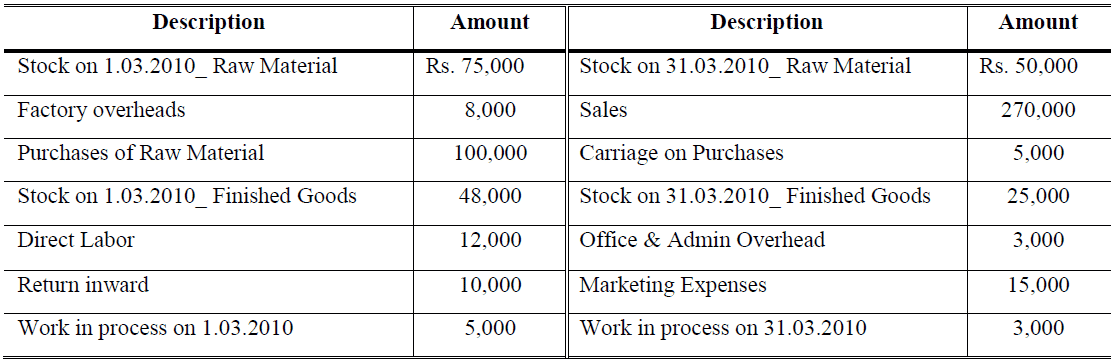

How do you think about the cost of goods sold?

Cost of goods sold formula At a basic level, the cost of goods sold formula is: Starting inventory + purchases − ending inventory = cost of goods sold. To make this work in practice, however, you need a clear and consistent approach to valuing your inventory and accounting for your costs.

How to calculate cost of goods sold (cog)?

Aug 08, 2021 · Beginning inventory + Purchases - Ending inventory = Cost of goods sold. Thus, if a company has beginning inventory of $1,000,000, purchases during the period of $1,800,000, and ending inventory of $500,000, its cost of goods sold for the period is $2,300,000.

How do you calculate cost of goods sold using periodic inventory?

Jul 13, 2016 · As you create a new item, you can simply add together the cost of all the supply units used in that good. The sum of these costs will get your “cost of goods made”, which I explained over in part 1. Keep a running log of the cost of …

What is not included in cost of goods sold?

What is cost of goods sold?

The cost of goods sold is the total expense associated with the goods sold in a reporting period. The cost of goods sold is subtracted from the reported revenues of a business to arrive at its gross margin.

What is charging to expense?

Charging to expense the difference between standard and actual costs for materials, labor, and overhead. There can also be differences in the cost of goods sold under the cash method and accrual method of accounting, since the cash method does not recognize expenses until the related supplier invoices are paid.

Does cost of goods sold include administrative expenses?

The cost of goods sold does not include any administrative or selling expenses. In addition, the cost of goods sold calculation must factor in the ending inventory balance. If there is a physical inventory count that does not match the book balance of the ending inventory, then the difference must be charged to the cost of goods sold.

What is cost of goods sold?

The Cost of Goods Sold is one of the important financial metrics and can be seen on the company’s profit and loss statement. This metric is used to subtract from the company’s revenues to estimate Gross Profit for any company. The Gross Profit Margin, which is Gross Profit/Revenues, is then used to estimate whether the company is efficiently utilizing its production processes and its labour. Any increases in the COGS might indicate that the company has to bear high raw material costs or increased labour costs, which might affect its bottom line.

What are the direct costs associated with COGS?

Taking an example, for a company like Ferrari, the direct costs that can be associated with COGS are the parts that go in making a Ferrari car and the labour costs used to manufacture it.

Why is it important to know how much a product cost you to make?

Because it’s important to know how much your products cost you to make. If you know how much a product cost you to create, then you can price it more accurately. That means you can better ensure that your biz is actually covering costs and making a profit. For more about pricing for a profit, see my article here.

What is COGS on tax return?

In the first case, ending inventory is your calculated amount. In the second case (on your tax return), COGS is your calculated amount. So just know and understand that for tax purposes, COGS is a calculation.

Explanation of Cost of Goods Sold Formula

Significance and Use of Cost of Goods Sold Formula

- The Cost of Goods Sold is one of the important financial metrics and can be seen on the company’s profit and loss statement. This metric is used to subtract from the company’s revenues to estimate Gross Profit for any company. The Gross Profit Margin, Gross Profit/Revenues, is then used to estimate whether the company is efficiently utilizing its p...

Cost of Goods Sold Formula in Excel

- Here we will do the same example of the Cost of Goods Sold formula in Excel. It is very easy and simple. You need to provide the three inputs, i.e. Beginning Inventory, Purchases during the year andEnding Inventory You can easily calculate the Cost of Goods Sold using the Formula in the template provided.

Conclusion

- Cost of Goods is an important metric that is used to determine Gross Profit for a company. Different accounting methodologies such as FIFO, LIFO, and Average Cost method determine the beginning and ending inventory for a company. The inventory measurement is then used to calculate the Cost of Goods Sold for a company. Therefore, investors need to take special care i…

Recommended Articles

- This has been a guide to a Cost of Goods Sold formula. Here we discuss its uses along with practical examples. We also provide you with the Cost of Goods Sold Calculator with a downloadable excel template. You may also look at the following articles to learn more – 1. Guide to Rule of 72 2. Formula for Inventory Turnover Ratio 3. Calculate Net Working Capital Using For…

Popular Posts:

- 1. which institute is best for medical transcription course in bangalore

- 2. what is financial management course

- 3. what is the best lsat prep course to take

- 4. how to write a college course curriculum

- 5. how long is billing and coding course

- 6. how long is medical assistant course

- 7. what is pmp training course

- 8. what is a course management system

- 9. what is business management course

- 10. how long is hvac course