What is asset turnover?

Asset turnover is a financial ratio that measures the value of revenue. Revenue Streams Revenue Streams are the various sources from which a business earns money from the sale of goods or provision of services. The types of.

What is the Purpose of the Asset Turnover Ratio?

The asset turnover ratio is a good indicator for measuring the health of a business and how efficient a company is in utilizing its assets to generate revenue. The higher the ratio, the better the business is performance-wise. On the other hand, a lower ratio may indicate a problem with one or more asset categories comprising total assets – inventory, receivables, or fixed assets.

How to calculate average total assets?

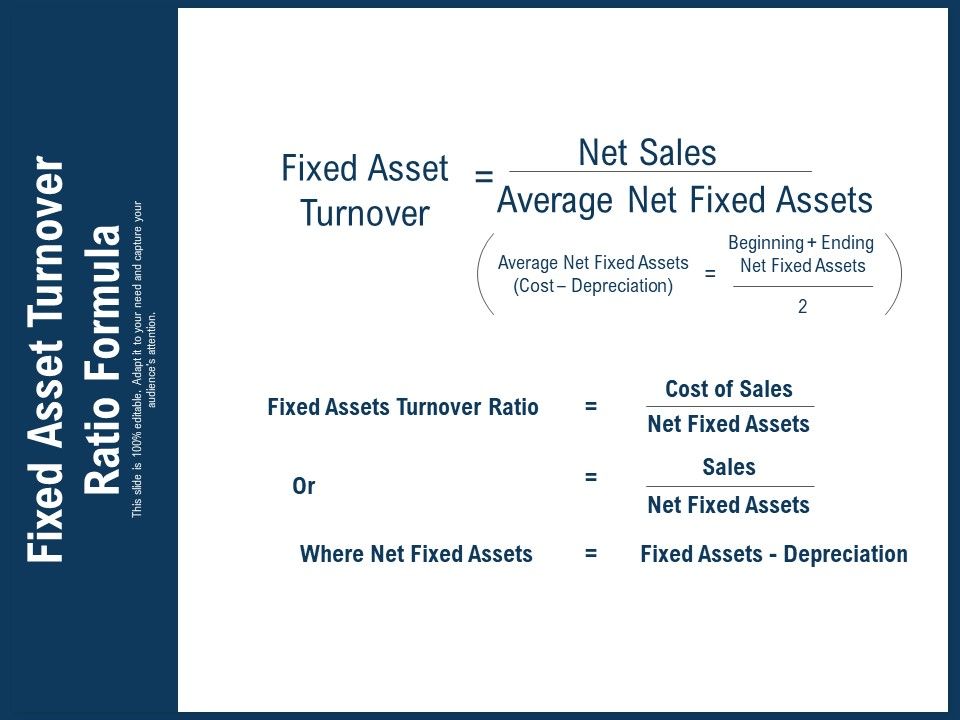

To calculate the average total assets, the beginning and ending asset balances are taken into consideration. The figures are then divided in half to get the average amount of assets owned by the company for a given fiscal or calendar year.

What is FAT in accounting?

Fixed Asset Turnover Fixed Asset Turnover (FAT) is an efficiency ratio that indicates how well or efficiently the business uses fixed assets to generate sales. This ratio divides net sales into net fixed assets, over an annual period. The net fixed assets include the amount of property, plant, and equipment less accumulated depreciation

When should the gain or loss from an involuntary conversion not be recognized?

c. The gain or loss from an involuntary conversion should not be recognized when the enterprise reinvests in replacement assets.

How much did Mendenhall Corporation cost to build a building?

Mendenhall Corporation constructed a building at a cost of $14,000,000. Weighted average accumulated expenditures were $5,600,000, actual interest was $560,000, and avoidable interest was $280,000. If the salvage value is $1,120,000, and the useful life is 40 years, depreciation expense for the first full year using the straight-line method is

How much did Wilson Co. pay for the land?

Wilson Co. purchased land as a factory site for $1,350,000. Wilson paid $120,000 to tear down two buildings on the land. Salvage was sold for $8,100. Legal fees of $5,220 were paid for title investigation and making the purchase.

What happens if a corporation purchases land and building and subsequently tears down the building and uses the property as?

If a corporation purchases land and building and subsequently tears down the building and uses the property as a parking lot, the proper accounting treatment of the cost of the building would depend on

When funds are borrowed to pay for construction of assets that qualify for capitalization of interest, the excess funds not needed to?

When funds are borrowed to pay for construction of assets that qualify for capitalization of interest, the excess funds not needed to pay for construction may be temporarily invested in interest-bearing securities. Interest earned on these temporary investments should be

How much did Nelson Corporation purchase land for?

On February 1, 2017, Nelson Corporation purchased a parcel of land as a factory site for $320,000. An old building on the property was demolished, and construction began on a new building which was completed on November 1, 2017. Costs incurred during this period are listed below: Demolition of old building $ 20,000 Architect's fees 35,000 Legal fees for title investigation and purchase contract 5,000 Construction costs 1,390,000 (Salvaged materials resulting from demolition were sold for $10,000.) Nelson should record the cost of the land and new building, respectively, as

What is asset turnover measuring?

The asset turnover ratio measures the efficiency of a company's assets in generating revenue or sales. It compares the dollar amount of sales (revenues) to its total assets as an annualized percentage. Thus, to calculate the asset turnover ratio, divide net sales or revenue by the average total assets. One variation on this metric considers only a company's fixed assets (the FAT ratio) instead of total assets.

Which sector has the highest average asset turnover ratio?

Retail and consumer staples, for example, have relatively small asset bases but have high sales volume—thus, they have the highest average asset turnover ratio. Conversely, firms in sectors such as utilities and real estate have large asset bases and low asset turnover.

How can a company improve its asset turnover ratio?

A company may attempt to raise a low asset turnover ratio by stocking its shelves with highly salable items, replenishing inventory only when necessary, and augmenting its hours of operation to increase customer foot traffic and spike sales. Just-in-time (JIT) inventory management, for instance, is a system whereby a firm receives inputs as close as possible to when they are actually needed. So, if a car assembly plant needs to install airbags, it does not keep a stock of airbags on its shelves, but receives them as those cars come onto the assembly line.

Can asset turnover be gamed by a company?

Like many other accounting figures, a company's management can attempt to make its efficiency seem better on paper than it actually is. Selling off assets to prepare for declining growth, for instance, has the effect of artificially inflating the ratio. Changing depreciation methods for fixed assets can have a similar effect as it will change the accounting value of the firm's assets.

Why is asset turnover deflated?

The asset turnover ratio may be artificially deflated when a company makes large asset purchases in anticipation of higher growth. Likewise, selling off assets to prepare for declining growth will artificially inflate the ratio. Also, many other factors (such as seasonality) can affect a company's asset turnover ratio during periods shorter than a year.

Why is asset turnover ratio higher?

The higher the asset turnover ratio, the better the company is performing, since higher ratios imply that the company is generating more revenue per dollar of assets. The asset turnover ratio tends to be higher for companies in certain sectors than in others.

What does it mean when a company has a low asset turnover ratio?

Conversely, if a company has a low asset turnover ratio, it indicates it is not efficiently using its assets to generate sales.

Popular Posts:

- 1. which institute is best for medical transcription course in bangalore

- 2. what is financial management course

- 3. what is the best lsat prep course to take

- 4. how to write a college course curriculum

- 5. how long is billing and coding course

- 6. how long is medical assistant course

- 7. what is pmp training course

- 8. what is a course management system

- 9. what is business management course

- 10. how long is hvac course