They are (parens includes date of full implementation, asterisk indicates states where law passed in 2022):

- Alabama (existing)

- *Florida (2027)

- *Georgia (2025)

- Iowa (existing)

- *Michigan (2028)

- Mississippi (existing)

- Missouri (existing)

- Nebraska (2024)

States requiring personal finance coursework in 2020:

Alabama, Arizona, Georgia, Idaho, Iowa, Kentucky, Michigan, Mississippi, Missouri, New Hampshire, New Jersey, New York, North Carolina, North Dakota, Ohio, South Carolina, Tennessee, Texas, Utah, and Virginia.May 13, 2022How many states require financial literacy courses?

The big picture: In all, 14 states mandate personal finance education at the high school level. Here's a breakdown of those states, according to the Next Gen Personal Finance, which offers personal finance curriculum.

Which states are the most financially literate?

Most Financially Literate States Michigan, Arizona, Virginia, and Tennessee make the grade when it comes to financial literacy.

Which states require economics in high school?

Alabama, Mississippi, Missouri, North Carolina, Tennessee, Utah and Virginia require high school students to take at least one semester of a personal finance course before graduation; one is currently implementing the requirement (Iowa); and four (Florida, Nebraska, Ohio and Rhode Island) are preparing to implement it ...

Is financial literacy required in Florida?

On March 22, Gov. Ron DeSantis, R-Florida, signed a bill that mandates a financial literacy course for high school students, making Florida the largest state to require one. Prior to this, the bill passed the Florida Congress unanimously.

How much of America is financially literate?

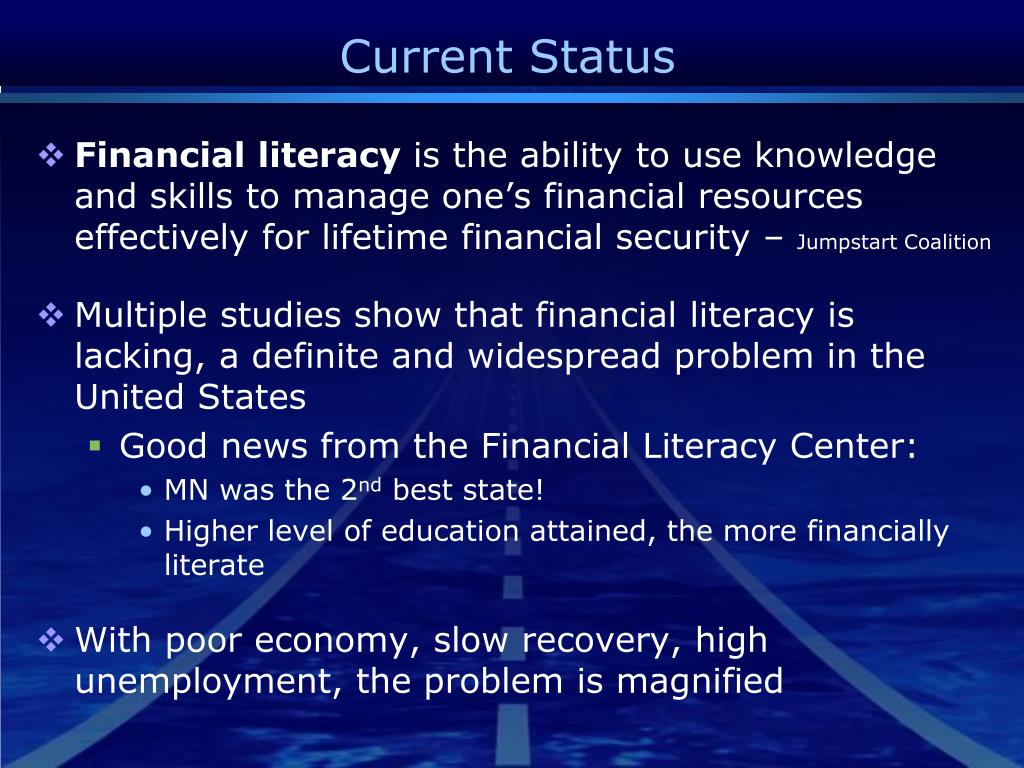

Only 57% of adults in the United States are financially literate, according to the Milken Institute. While a majority of parents say they are responsible for teaching children about finances, 31% say they never talk to their children about the topic, according to a CNBC + Acorns and Momentive survey.

What is wallet literacy?

Being financially literate means you understand the core concepts of money management and are able to apply them in a manner beneficial to your family's long-term financial comfort and security. So complete the test, get your WalletLiteracy Score and use it to secure a richer financial future!

Is financial literacy taught in schools?

Basic financial skills are generally not taught in classrooms in the United States. A lack of financial education has led to Americans having inadequate household and retirement savings and high levels of credit card and student loan debt.

Is financial literacy required in NJ?

The State of New Jersey requires ALL high school graduates to complete 2.5 credits (one semester) in Financial Literacy. Both District High Schools offer courses that meet this requirement through the Business and the Family and Consumer Science Departments.

Why are people not financially literate?

Financial illiteracy is more common among low-income individuals because they typically do not have wide access to accurate financial information. With such illiteracy, youth in low-income households can fall victim later as adults to scams, high-interest rate loans, and increasing debt.

What classes are required to graduate high school in Florida?

The course credits required to graduate include:English/Language Arts: 4 credits.Math: 4 credits.Science: 3 credits.Social studies: 3 credits.Fine and Performing Arts, Speech and Debate, or Practical Arts: 1 credits.Physical Education: 1 credit.Elective Courses: 8 credits.

Who wrote the financial literacy bill in Florida?

The bill was introduced in the Senate by District 7 Sen. Travis Hutson, who represents Flagler County, St.

What month is Financial Literacy Month?

AprilThe United States Senate passed a resolution in 2003 officially designating April as Financial Literacy Month. President Obama made a proclamation in March 2017 highlighting the importance of being financially capable and declaring the month of April as National Financial Capability Month.

Should economics be required in high school?

So the first reason that students should learn economics is to help them make the connection between hard work and success in school and in life. Economics is not as important as reading and math; it is more important because it gives students a reason to learn to read and to conquer algebra and other math skills.

What is taught in high school economics?

Students go on to explore both micro- and macroeconomics, the laws of supply and demand, and important economic policies. A chapter dedicated to global economies helps students understand concepts like international trade, currency and how exchange rates work, and globalization.

Is economics a difficult subject?

Even though economics is a social science, it can be as difficult and demanding as any of the more challenging academic subjects, including math, chemistry, etc. To do well in economics requires time, dedication, and good study habits.

What credits do I need to graduate high school in Texas?

HOW MANY CREDITS ARE NEEDED TO GRADUATE HIGH SCHOOL IN TEXAS? Students must successfully earn a minimum of 26 credits to graduate and also pass state tests.

Why do we live where we live?

Ultimately, you live where you live for any number of reasons -- roots, family, employment, weather, and so on. If you’re fortunate enough to live in a state that stresses financial literacy in schools and whose residents are well-informed about financial and investment matters, you have an advantage when it comes to finance smarts.

Why do some people make good financial decisions while others make poor ones?

What causes some of us to make good financial decisions while others make poor ones? In many cases, it’s the level of financial literacy we have.

What are the areas of financial literacy?

budgeting, investing, insurance, college funding, saving for retirement, and. tax planning. Financially literate people make better choices in all these areas. While it’s easy to understand the concept of financial literacy, attaining it is another story. In fact, about two-thirds of American adults can’t pass a basic financial literacy test.

What factors contribute to financial literacy?

Demographic, social, familial, and personal factors all play a role in one’s development of strong financial literacy skills. But geography may also be relevant. Consider the list below. If you live in one of these states, you and your co-residents are leading the country in financial smarts.

How many states require personal finance courses?

In our country’s high schools, financial education is, to use a non-technical term, all over the place. Currently, 17 states require a personal finance course to graduate high school.

What is CashCourse.org?

CashCourse.org, from the National Endowment for Financial Education, provides free online education courses, customizable financial tools, and more.

Which states have the gold standard in financial education?

(Those states are Alabama, Arkansas, Georgia, and Texas.) Bottom states financial literacy - Infogram.

How many states have personal finance requirements?

So, it would appear that 15 of the 21 states counted as having a Personal Finance requirement in this report actually embed personal finance standards into another course. In reality, this means that a course that has just a week or two (or even less) of personal finance content embedded would be considered a state where a student is required to take a personal finance "course" [quotations are mine].

What is the gold standard for financial education?

In order to be considered "Gold Standard" a state must guarantee that all students will take a one-semester Personal Finance course before they graduate from high school. I'm going to get a little wonky here to highlight why we hold states to a high standard when it comes to providing financial education.

Why did Kentucky change the language at the final moment from a personal finance "course" to a "program?

Kentucky -- changed the language at the final moment from a personal finance "course" to a "program," an incredible loophole because "program" was never defined. The reality on the ground is that it's often a race to the bottom in too many districts where they are taking the stance that a three-hour online module will satisfy this requirement.

How did Tim start his savings?

Tim's saving habits started at seven when a neighbor with a broken hip gave him a dog walking job. Her recovery, which took almost a year, resulted in Tim getting to know the bank tellers quite well (and accumulating a savings account balance of over $300!). His recent entrepreneurial adventures have included driving a shredding truck, analyzing executive compensation packages for Fortune 500 companies and helping families make better college financing decisions. After volunteering in 2010 to create and teach a personal finance program at Eastside College Prep in East Palo Alto, Tim saw firsthand the impact of an engaging and activity-based curriculum, which inspired him to start a new non-profit, Next Gen Personal Finance.

How many states require personal finance courses?

This, in turn, has led to a lot of inquiries as to why NGPF's Got Finance? research report on access to financial education finds that only 6 states require students to take a personal finance course before they graduate ( our State Legislative Pocket Guide has all the details ). I thought it would be useful to explain how we arrived at our numbers.

Is a personal finance course more likely to stick?

One semester: research finds that "students learn by doing" so a Personal Finance course, rich with hands-on activities and simulations that are relevant to a students' lives, is more likely to stick . This type of course simply takes more time to teach well. In addition, the scope of a Personal Finance course that is relevant to a high schooler is quite comprehensive and should not be short-changed by anything less than a full semester.

Have you seen the documentary The Most Important Class You Never Had?

Have you seen the documentary The Most Important Class You Never Had? We created this for teachers to share with their community, to inspire efforts to guarantee every student graduates high school taking a personal finance class.

What is the coalition website?

The coalition’s website includes a clearinghouse of instructional material for teachers, often free. Some programs are sponsored by financial institutions, Ms. Levine said, but the coalition requires that the material be presented in a “balanced” way.

What is a report card in high school?

The report card, an update of an assessment done in 2015, is based on the premise that all high school students should, at a minimum, be required to take a course that includes personal finance topics, even if the topics are just a “modest” part of the overall course.

Why are parents hesitant to make a budget?

Parents may be hesitant because they have made poor decisions themselves in the past, Ms. Levine said. Still, she said, parents should try to talk about spending and budgeting — starting, perhaps, by explaining why the family made a certain budget decision. Or, she suggested, parents could research, together with their children, information about setting savings goals. The coalition offers tips and online tools on its website.

Which states have financial literacy?

The 2017 Financial Report Card from Champlain College’s Center for Financial Literacy gave just five states — Alabama, Missouri, Tennessee, Utah and Virginia — an A grade for their efforts. The five require high school students to take at least a half-year personal finance course, or the equivalent, as a graduation requirement.

Which state has the only A+?

Utah was the only state to get an A-plus. The state requires students to take a state-administered test at the end of the course, and recently mandated that the class cover the cost of college and student loans.

Does financial education improve financial well-being?

The authors of a separate study, done in 2015 and funded by the Finra Investor Education Foundation, noted that past research had found, “at best, mixed evidence” that financial education improved financial well-being. Still, after comparing three states that adopted mandatory personal finance instruction with neighboring states that did not, the study found reason for optimism.

Who is Professor Willis?

Professor Willis is advising the FoolProof Foundation, a Florida nonprofit group that creates free courses that teach high school students (and now middle school students) the importance of a “healthy skepticism” when evaluating various forms of debt.

Popular Posts:

- 1. which institute is best for medical transcription course in bangalore

- 2. what is financial management course

- 3. what is the best lsat prep course to take

- 4. how to write a college course curriculum

- 5. how long is billing and coding course

- 6. how long is medical assistant course

- 7. what is pmp training course

- 8. what is a course management system

- 9. what is business management course

- 10. how long is hvac course